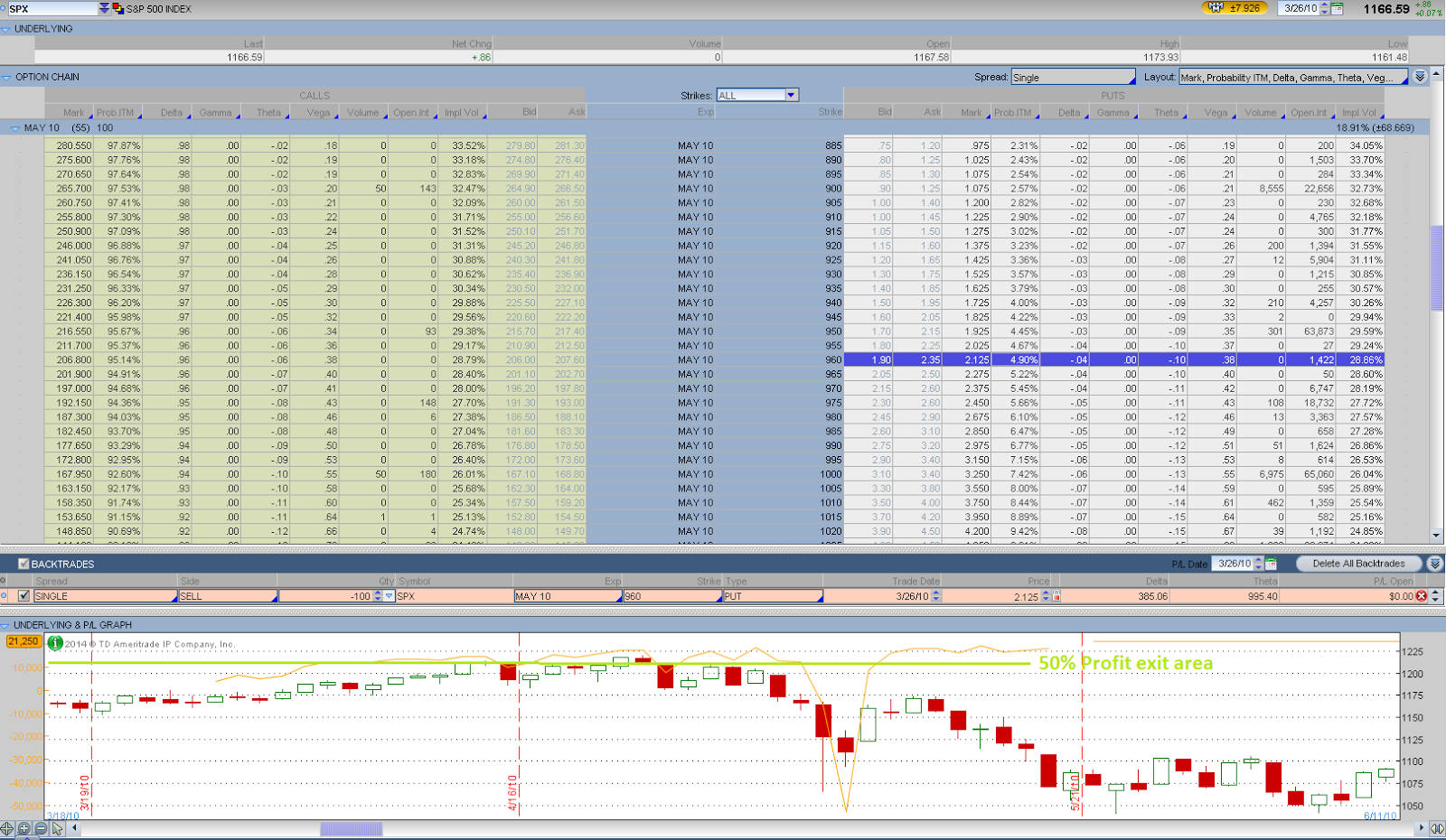

I've been interested in studying the trading

process and

mindset of successful traders. Today, I reviewed what I learned from Karen's interviews from the trading process perspective.

Karen treats trading as a process

and manages the process all the time. As far as I can see, her trading process involves

the following elements as discussed in her interviews:

o

A suitable set of strategic trading rules,

o

An advanced trading software platform,

o

A successful trading mindset and psychology,

o

A daily trading routine,

o

A trading number game management,

o

An experienced trading team,

o

A Sufficient amount of time and money for

trading and learning, and

o

Others.

Karen’s daily trading routine

starts from market open hour till the end. The constant watch on the market by

her trading team allows them to react to market changes promptly. Karen’s

trading rules help them staying away from over-trading or over-adjusting. Her

high degree of confidence on the high probability trades enables her of proper

trade actions in the face of market uncertainty.

Karen treats trading as a number’s

game so that she can play it objectively. She enjoys playing the big game all

the time and taking the market challenges as well. There are no feelings

wrapped around her trades or positions, as they are just numbers to her. The

ability to turn emotions and perceived risks into a set of trading numbers and

to focus on the numbers helps traders to decouple themselves from emotions and

irrational trading actions. The emotion and fear are the biggest obstacles in

trading and they take down most traders. The focus on trading numbers takes

away the feeling of heart-ripping during adverse market conditions. As a result

of the application of high probability trades by going far out of the money, a

heavy percentage of Karen’s positions are winners.

Karen had discussed her learning

and trading improvement process. She had more failures than successes in

initial years. She was willing to invest in learning knowledge with a large

amount of money and time that many other people may not be comfortable with.

Her education fee at Investools alone cost over 20K USD. Small traders may have

this limited amount in their trading accounts.

Karen established a tremendous

trading team of about 6 members. 5 of them are experienced retail traders and 1

is an accountant. She encourages different ideas from team members. They

usually will listen to each other, discuss the ideas and agree as a group. From

time to time, they will test water with new ideas using a small amount of

capital. If the new idea is proven to be working, then they don’t hesitate to

apply it in full scale. The selling of weekly option was a good example of this

process of adopting new ideas.

Some traders may get extremely

disturbed if the temporary position loss becomes very big. Karen does not get

emotional about any of her positions. When positions are in danger, she will do

whatever it takes to fix them and make them back to the original profit at the

expiration date as described in Section 6

Trade

Adjustment Rules.

She is not bound by the future direction of market moves, but always reacts to

it if the ITM probability and profit percentage of her positions indicate to

her for adjustments.

Karen suggested traders to look at

the profit and loss numbers of the portfolio but not to focus on the P&L.

This is reflected on her trading team structure as well as there is only one

accountant (vs 5 to 6 traders). With this team, the traders should be able to

focus more on the other important trading numbers. Personally, I think the key numbers

Karen discussed in the interviews can be summarized as the following:

·

ITM probability

o

First factor used to determine if opening,

closing or adjustment is required

·

Prices and trend of the underlying

o

Second factor used to determine if adjustment is

required

·

Stress-tested market crash losses vs net

liquidation value

o

Critical number that indicate how many contracts

to sell

·

Option premium changes and time to expiration

o

Available options for adjustments

Karen stated she is willing to

take losses when necessary and she will keep existing profit in her positions

also. However, there were no examples discussing when to give up positions for

losses (probably after the portfolio margin runs out). It’s worthwhile noting

that Karen did not indicate any rules based on position losses. She did not

mention any direct trade reaction to the amount of loss of a position. Her

trade adjustment rules are based on ITM probability and the current market

trends.